- Surmount Markets

- Posts

- The Hormuz Bottleneck: Why the Energy Shock May Only Be Getting Started

The Hormuz Bottleneck: Why the Energy Shock May Only Be Getting Started

With the Strait of Hormuz effectively locked down, global energy security has shifted from a policy debate to a structural crisis—and the market’s reliance on emergency reserves is a gamble that may already failing

Logan Weaver

March 13, 2026

In partnership with

If you were looking for signs that the volatility in the Gulf might subside, the events of this week have provided a sobering reality check. Following the U.S. and Israeli joint military campaign which almost immediately brought down the Iranian regime’s Supreme Leader, the expected "shock and awe" pacification of the region has instead triggered a desperate, asymmetrical counter-offensive.

Iranian counter-attacks have expanded beyond traditional military targets to explicitly weaponize global energy transit. In a span of just 72 hours, we have seen a surge in kinetic strikes against commercial vessels and energy infrastructure, including fuel storage facilities at the Port of Salalah and direct projectiles hitting tankers in the Arabian Gulf.

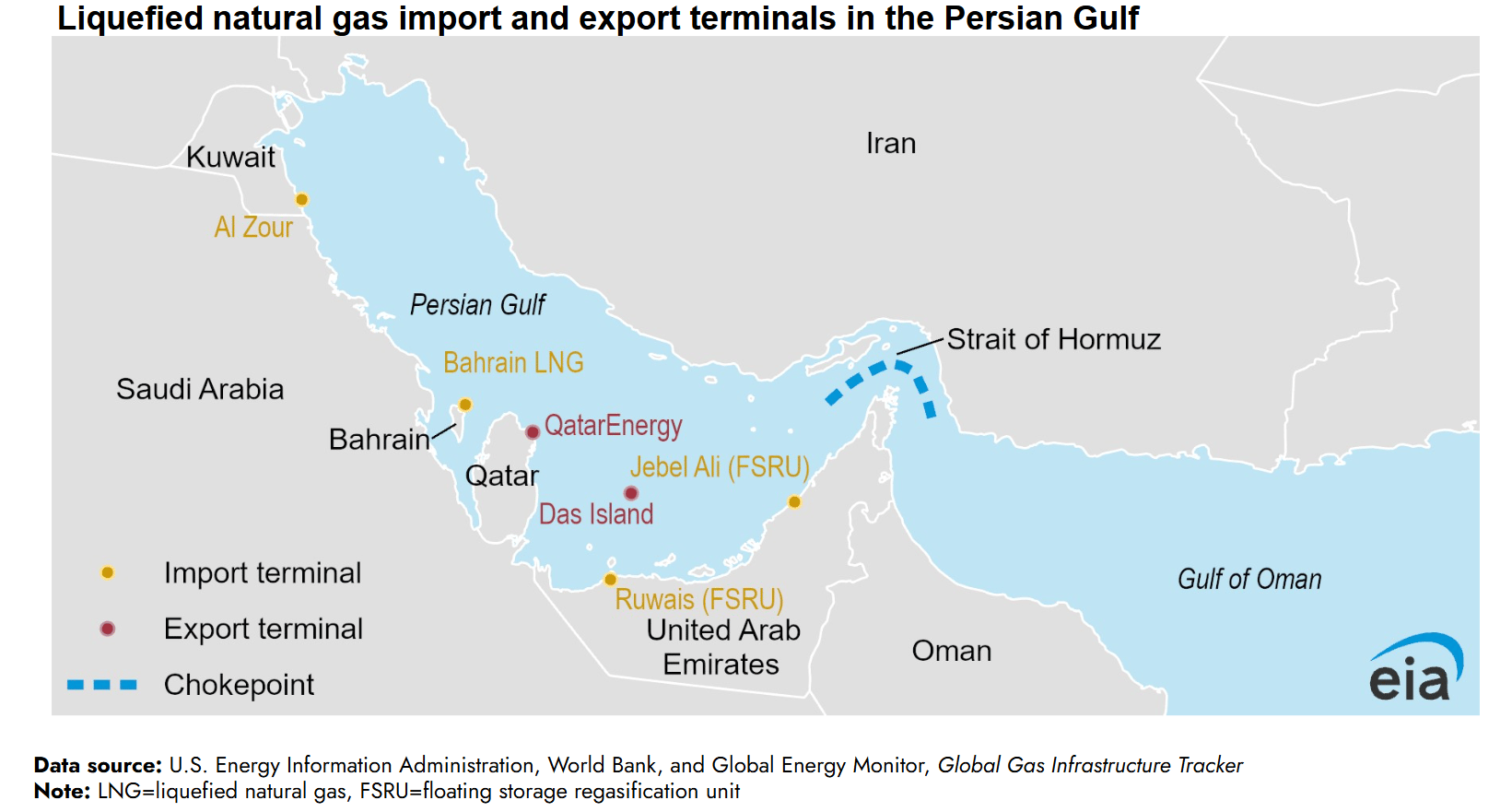

Most critically, the effective strangulation of the Strait of Hormuz—the artery for roughly 20 million barrels per day—has transitioned from a high-risk threat to a functional reality.

As Iran’s new leadership doubles down on using this maritime chokepoint as its primary geopolitical lever, the market’s reliance on "temporary" fixes has been exposed. While policymakers scramble to announce record-breaking releases from strategic petroleum reserves, the hard math of global consumption suggests these are merely stopgaps for a crisis that is structural, not cyclical. We are no longer watching a headline-driven skirmish; we are witnessing the onset of the most significant energy supply disruption in modern history.

Find out why 200K+ engineers read The Code twice a week

Staying behind on tech trends can be a career killer.

But let’s face it, no one has hours to spare every week trying to stay updated.

That’s why over 200,000 engineers at companies like Google, Meta, and Apple read The Code twice a week.

Here’s why it works:

No fluff, just signal – Learn the most important tech news delivered in just two short emails.

Supercharge your skills – Get access to top research papers and resources that give you an edge in the industry.

See the future first – Discover what’s next before it hits the mainstream, so you can lead, not follow.

The Extent of the Global Oil Supply Paralysis

While we are only two weeks into this conflict, it certainly does appear that we are currently witnessing the most severe maritime energy disruption in modern history.

The Strait of Hormuz is a central nervous system of global energy. With the passage effectively shuttered, the market is no longer dealing with a supply "hiccup"—we are facing a structural severance of the global energy supply chain

To understand the gravity of this paralysis, we must move beyond the rhetoric of "market volatility" and look at the physical mechanics of the flow. Normally, approximately 20 million barrels per day (bpd) of crude oil and petroleum products—roughly 20% of global consumption—transit this narrow 21-to-33-kilometer corridor.

As of mid-March 2026, the Strait is functionally closed. While nominal traffic exists, it is a shell of its former self, with transit volumes plummeting to near-zero levels. This isn't just about ships waiting in line; it is about the fundamental inability of the world’s largest oil-producing region to move its product to market via its primary export artery.

The Illusion of "Alternative Routes"

Market analysts often point to existing pipelines—such as Saudi Arabia’s East-West pipeline—as a natural pressure-release valve. By rerouting crude oil from eastern fields to the Red Sea port of Yanbu, Saudi Arabia can maintain critical exports even when its primary Gulf routes are inaccessible.

However, the current crisis exposes the limits of this "redundancy." Even at full capacity, these land-based bypasses can only handle 7 million bpd, out of which 5 million are allocated for export purposes. As such these are not a replacement for the massive maritime throughput required to feed global energy demand; they are, at best, a minor mitigation strategy for a catastrophe of this scale.

The Kinetic Risk & The "Dark" Fleet

The risk environment has fundamentally shifted from a geopolitical standoff to a kinetic war zone. With multiple commercial vessels sustaining damage from drones and missiles—and reports of Iranian naval mines being deployed—the waterway has effectively become a high-risk insurance black hole.

Major insurers have issued notices of cancellation for Gulf waters, and war-risk premiums have surged, rendering standard commercial shipping through the area economically unfeasible, even if vessels were willing to brave the physical danger.

Beyond Crude: The Multi-Commodity Shock

The paralysis extends beyond crude oil. Roughly 25% of the world’s Liquefied Natural Gas (LNG) trade also transits this passage.

We are witnessing a dual-fuel shock where the physical inability to move energy is decoupling from historical pricing models. As stocks dwindle and the prospect of a swift reopening fades, the global market is shifting from a price-discovery phase to a physical-shortage phase—where the primary question is no longer "what is the price?" but "is the supply actually available?"

Why Strategic Reserves Are Not The Solution They Seem

The recent, historic coordinated release of 400 million barrels of crude by the International Energy Agency (IEA) was billed as the definitive market stabilizer—a "firebreak" meant to calm soaring prices and patch the holes in the global supply chain. But when we strip away the headline-grabbing numbers, the math reveals a much more sobering reality: these reserves are a temporary psychological buffer, not a structural solution.

To understand why this relief is largely illusory, we have to look at the scale of the disruption in the Strait of Hormuz.

The Math of Consumption: Consider the U.S. contribution to this effort. The release of 172 million barrels from the Strategic Petroleum Reserve (SPR) sounds substantial in a vacuum. Yet, with domestic consumption hovering at roughly 20 million barrels per day, this entire cache covers less than nine days of total U.S. demand.

A Drop in the Ocean: When we zoom out to the global stage, the 400 million barrel total represents a fraction of the daily volume (20M bpd) that typically flows through the Strait. If that artery remains compromised, the global market is effectively staring down a supply deficit that no amount of stored crude can bridge for more than a few weeks.

The market has been quick to interpret these releases as "mission accomplished," allowing oil prices to pull back from the brink. However, investors should be wary of confusing liquidity for solvency. Strategic reserves are designed for short-term price smoothing during temporary outages—they were never intended to compensate for the total, indefinite closure of the world’s most critical maritime energy chokepoint.

As long as the security situation in the Gulf remains volatile, the market is betting on a safety net that is rapidly thinning. Once this temporary supply is exhausted, the structural deficit will remain, leaving the market highly vulnerable to a sharp, aggressive price correction.

The New Oil Price Floor

For years, oil markets have been lulled into a sense of security by the expectation that supply disruptions are temporary—a "blip" that inventory releases or diplomatic pressure could resolve. The current situation in the Strait of Hormuz suggests that this paradigm is obsolete. We are no longer dealing with a temporary bottleneck; we are witnessing a structural shift that establishes a significantly higher price floor for global energy.

The market’s tendency to "buy the dip" based on the hope of a quick resolution is increasingly at odds with the reality on the ground. When approximately 20 million barrels per day—a massive share of global energy transit—faces systemic threats, the risk premium is no longer just a short-term volatility spike; it is potentially a permanent cost of doing business.

Why the Floor Has Moved Up

The Insurance & Logistics Tax: Even when tankers successfully navigate the Gulf, the cost of transit has fundamentally changed. Surging war-risk insurance premiums, higher freight rates, and the need for complex, time-consuming rerouting have effectively baked a "scarcity premium" into every barrel. These are not transitory costs; they are persistent expenses that refiners and end-consumers must now absorb.

The Erosion of Spare Capacity: The speed at which prices reacted to recent escalations highlights a troubling reality: the global "buffer" is thinner than many analysts presumed. As geopolitical risk clouds the reliability of Persian Gulf supply, the market is quickly moving from pricing in a logistics delay to pricing in a permanent, structural deficit.

Market Psychology and the "Risk of Re-escalation": Price floors are reinforced by the fear of what comes next. As long as the threat of infrastructure attacks remains, traders will maintain a significant hedge, refusing to push prices back to pre-crisis levels. The market is effectively pricing in the constant possibility of a total shutdown, making it extremely difficult for oil to trade back down to previous baseline levels without a credible, durable, and highly visible return to normalcy.

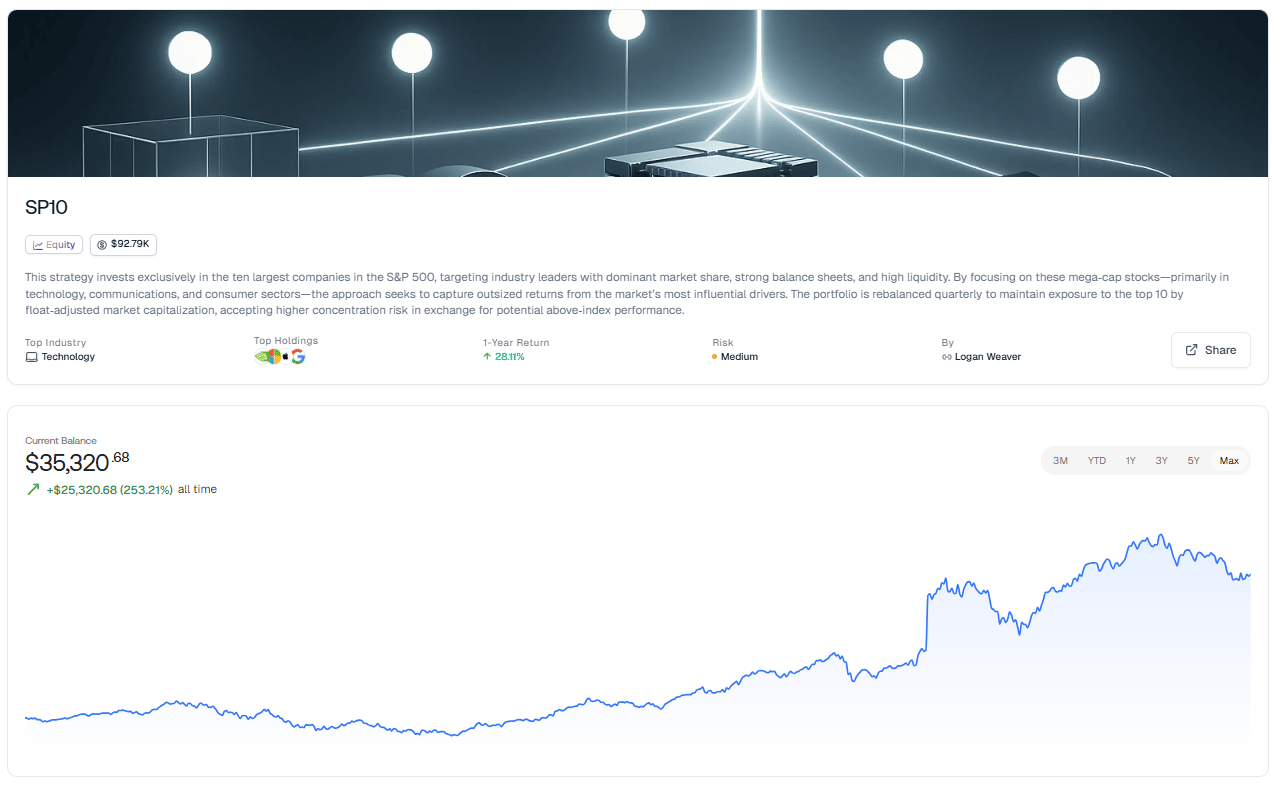

Why A "Flight to Quality" Makes Most Sense in Volatile Seas

When geopolitical instability sends commodity markets into a tailspin, the most dangerous thing an investor can do is "guess" at smaller, riskier plays. History shows that during systemic energy shocks, capital doesn't disappear—it migrates. It flows toward the "Fortress Balances"—the companies that are so large, so liquid, and so essential that they become the safe harbor of the global economy.

This is why the Surmount SP10 strategy is more relevant today than ever.

In an environment where supply chains are fracturing, you don’t want to be exposed to speculative volatility. You want to own the titans. The Surmount SP10 strategy is built on a simple, ironclad philosophy: In times of chaos, bet on the leaders.

Dominance as a Moat: By investing exclusively in the top 10 companies of the S&P 500, you are owning the undisputed kings of technology, communication, and consumer sectors. These companies possess the pricing power to weather inflationary pressures that crush smaller competitors.

The Power of the Fortress Balance Sheet: When energy costs spike and input prices rise, companies with massive cash piles and zero reliance on high-interest debt don't just survive—they thrive. They use their capital to expand, innovate, and buy market share while others are forced to retreat.

Dynamic Resilience: The SP10 isn't a "set it and forget it" index fund. We rebalance quarterly to ensure you are perpetually positioned in the current market leaders. Whether the market rotates or consolidates, your portfolio is locked into the most influential drivers of global growth.

Stop gambling on the periphery. When the macro outlook is uncertain, stop trying to find the next "hidden gem" and start owning the pillars of the global economy.

— Surmount Markets Team