- Surmount Markets

- Posts

- Markets Breathe Again: The $94 Oil Relief Rally, Improved Risk Appetite, and the AI Infrastructure Boom

Markets Breathe Again: The $94 Oil Relief Rally, Improved Risk Appetite, and the AI Infrastructure Boom

A global ceasefire has sparked a massive relief rally; inside, we cover the 2026 economic calendar, the 'death cross' in the S&P 500, and the surge in AI infrastructure

Logan Weaver

April 10, 2026

In partnership with

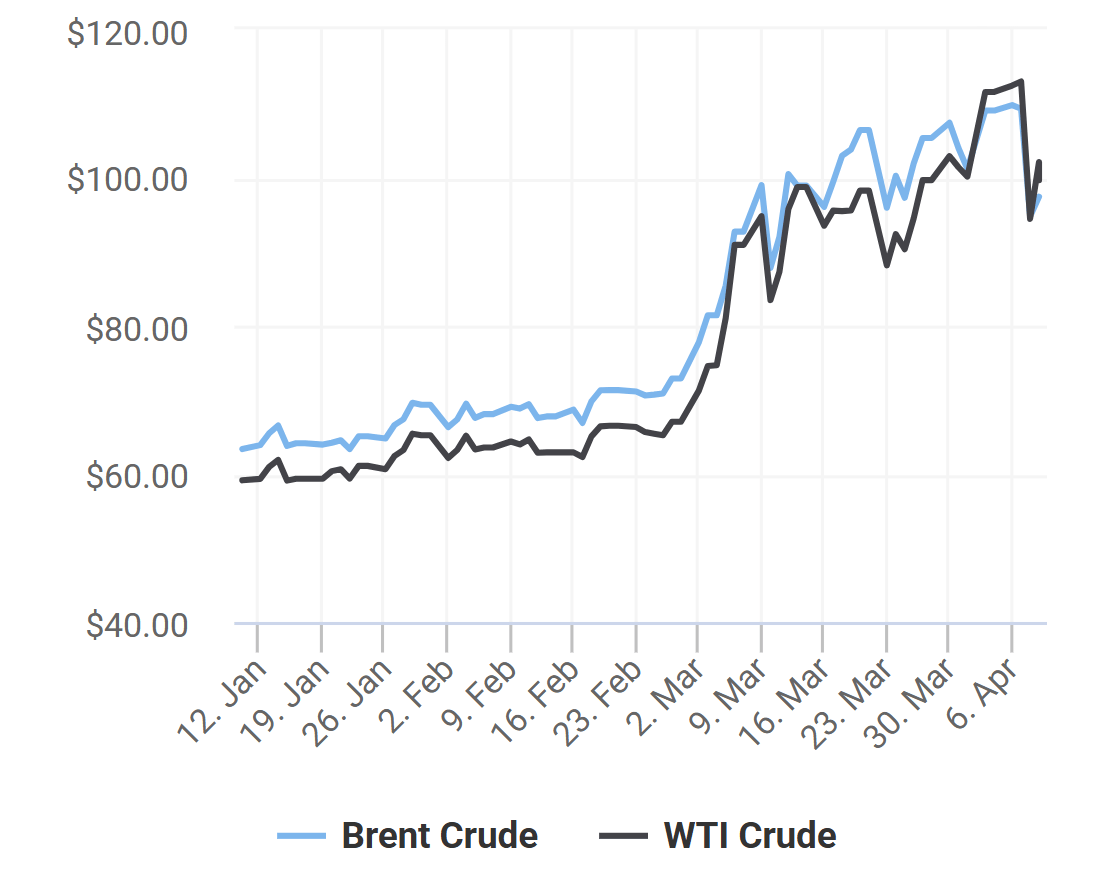

Oil prices plunged 15% earlier this week, which was the steepest single-day decline since April 2020, in a relief rally as supply disruption fears eased. West Texas Intermediate (WTI) fell to approximately $94.41 per barrel.

This, of course, had come on the heels of a geopolitical powder keg that threatened to melt down the global energy grid. President Trump had earlier threatened to pretty much annihilate Iran’s entire civilian infrastructure—from power plants to bridges—warning on Truth Social that a "whole civilization will die tonight" if the Strait of Hormuz remained closed.

But in a classic "art of the deal" twist, the world woke up to a different reality. Just two hours before the Tuesday night deadline, a Pakistan-mediated two-week ceasefire was agreed upon by both the American and Iranian sides. As a result, the market, almost immediately took on a relief rally that not only saw oil prices plunge to the $90 mark, but also a fall in the U.S. Dollar Index, which dropped 1.2% below 100, as investors rotated out of haven assets.

Tech moves fast, but you're still playing catch-up?

That's exactly why 200K+ engineers working at Google, Meta, and Apple read The Code twice a week.

Here's what you get:

Curated tech news that shapes your career - Filtered from thousands of sources so you know what's coming 6 months early.

Practical resources you can use immediately - Real tutorials and tools that solve actual engineering problems.

Research papers and insights decoded - We break down complex tech so you understand what matters.

All delivered twice a week in just 2 short emails.

This Weeks Economic Calendar 📅

The week of April 6–10, 2026, has been defined by a heavy Economic Calendar featuring critical inflation data, Federal Reserve insights, and high-impact geopolitical deadlines.

Tuesday, April 7:

Durable Goods Orders: Offered insights into business investment and economic momentum.

Wednesday, April 8:

FOMC Meeting Minutes: Released at 2:00 pm ET, providing nuanced clues on the Fed's stance regarding inflation and future interest rate cuts.

Thursday, April 9:

Core PCE Price Index (February): The Federal Reserve's preferred inflation gauge showed an annual increase of 3.0%, while the monthly rate was 0.4%.

Final Q4 2025 GDP: The US economy expanded at an annual rate of 0.5%, lower than the previously estimated 0.7%.

Initial Jobless Claims: Rose to 219,000, exceeding forecasts.

Friday, April 10:

Consumer Price Index (CPI) March: A high-impact release scheduled for 8:30 am ET to provide the latest snapshot of headline inflation.

University of Michigan Consumer Sentiment: Preliminary April reading released at 10:00 am ET.

Geopolitical & Market Headlines

Iran Deadline (April 6–7): Markets were highly sensitive to a deadline set by President Trump for Iran to reopen the Strait of Hormuz. Stocks initially rose on hopes of a 45-day ceasefire but remained volatile as the deadline passed.

Federal Initiatives: On Monday, shares of BNY Mellon and Robinhood rose following their selection to support the new "Trump Accounts" program for newborns.

Earnings Highlights

The first-quarter earnings season is ramping up with several notable reports this week:

Delta Air Lines (DAL): Reported this week, providing a look at travel demand and fuel cost impacts.

Levi Strauss (LEVI) & Constellation Brands (STZ): Also featured on the Earnings Calendar for early April.

BlackRock (BLK) & BlackBerry (BB): Among the major companies reporting results during this window.

Where Markets Stand 📊

If this week’s analysis has shown us anything, it’s that the "Buy and Hold" era of Bitcoin is being tested by a new, more complex economic reality. In a world of no ceasefires, shifting interest rates, and failing scarcity models, emotional trading is an investor's greatest liability.

S&P 500: The index is at a critical technical inflection point after a "death cross" pattern, with investors watching if it can hold its 200-day moving average amid recession fears.

VIX: Volatility spiked as the market was "on edge" ahead of geopolitical deadlines, but it has since retreated toward 20 as relief over a temporary ceasefire sets in.

Gold: Gold prices are up over 1% and trading near a three-week high as a weaker dollar, the fragile U.S.-Iran ceasefire, and anticipation of U.S. CPI data support the market.

Oil: Brent crude is the primary macro driver this week, swinging between $120 and $90 based on the fragility of the Middle East ceasefire and potential for permanent transit fees in the Strait of Hormuz.

BTC: Bitcoin surged back above $72,000 as a high-risk asset benefiting from the de-escalation of war, with further speculation fueled by reports that it could be used for regional transit payments.

Why Industrials and AI Infrastructure Are Leading the Ceasefire Rally

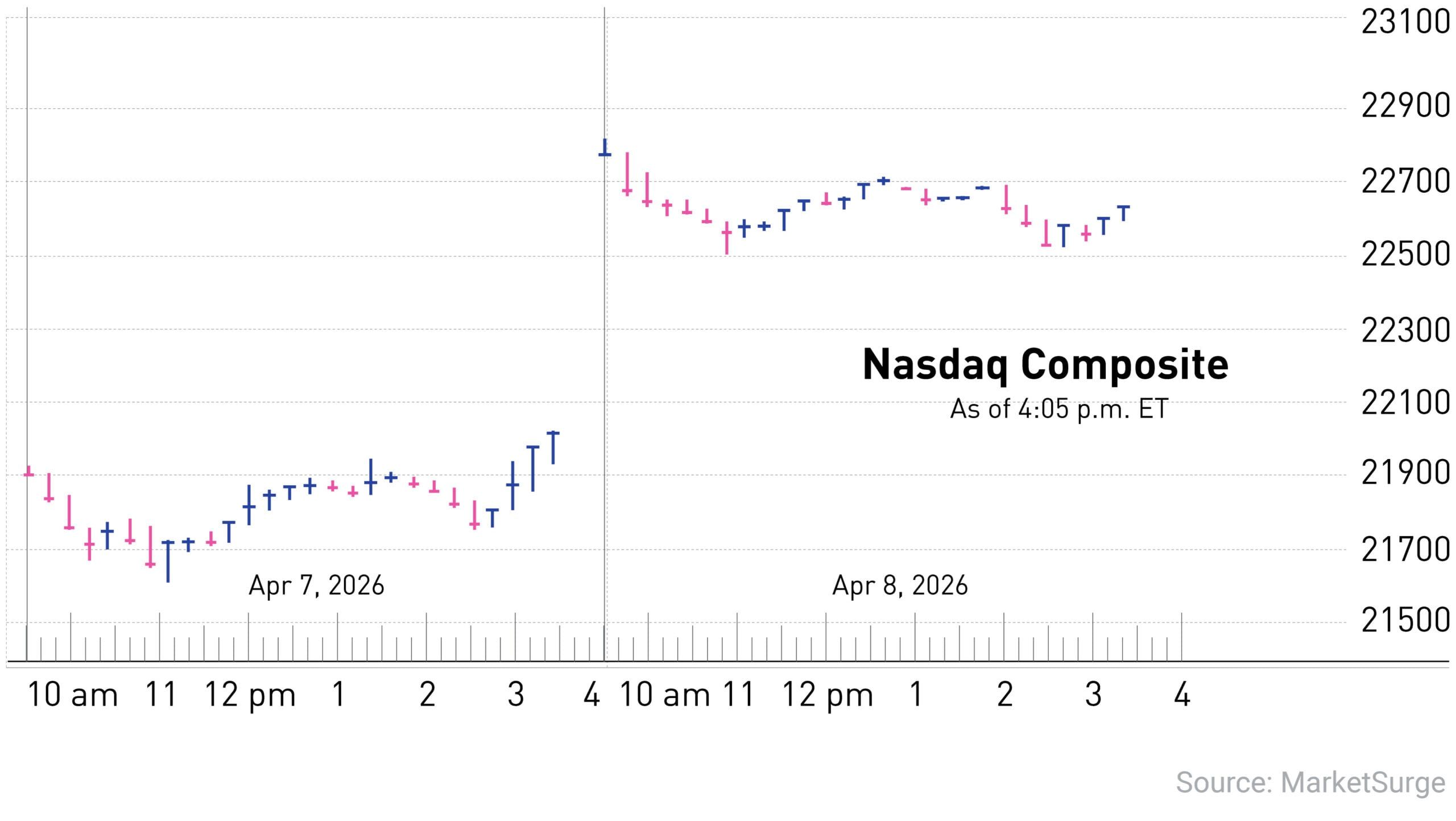

The two-week ceasefire seems to have reignited investor appetite for risk, as is evident from the surge seen across global equity markets, with the Nasdaq 100 jumping 2.5%, the S&P 500 rising 2.2%, and the Nikkei 225 climbing nearly 5%.

While the broader markets rallied on Wednesday, the following day highlighted that optimism remains tempered by a lingering "pain point", which is the Strait of Hormuz. Despite the truce, maritime traffic remains stalled, with only five transits recorded in the 24 hours following the announcement. However, with U.S. midterm elections approaching, political pressure to de-escalate suggests the market lows may finally be in the rearview mirror.

Industrials Step Into the Spotlight

While technology often dominates recovery headlines, the Industrials sector was Wednesday’s top performer. This sector is uniquely sensitive to shifting interest rate expectations and supply chain normalization. Despite the CME FedWatch Tool currently pricing in no rate cuts for 2026, the 2-year Treasury yield’s retreat from its March highs suggests the market is beginning to price in a more dovish pivot.

The rebound is bifurcated between temporary bounces and long-term structural shifts:

Tactical Bounces: Airlines and heavy machinery spiked on expectations of lower fuel costs and eased fertilizer shortages.

Structural Winners: Electrical Equipment and Specialty Industrial Machinery are the primary "picks and shovels" of the AI data center buildout.

Companies like Vertiv ($VRT ( ▲ 2.6% ) ) , nVent ($NVT ( ▲ 1.5% ) ), and GE Vernova ($GEV ( ▲ 2.41% ) ) are benefiting from a massive "transformer crunch." With over half of planned U.S. data centers facing delays due to equipment shortages, these asset-heavy businesses are seeing a sharp re-rating as they shore up the nation's aging power grid.

The AI Infrastructure Trade

Within Tech, investors are shifting away from "obvious" plays like Nvidia ($NVDA ( ▲ 2.57% ) ) in favor of semiconductor equipment and memory. Applied Materials and Lam Research remain favored for their exposure to HBM and DRAM production, essential for AI scaling. Conversely, software giants like Microsoft ($MSFT ( ▼ 0.59% ) ) have seen a more sluggish recovery, suggesting that the market’s immediate confidence lies in the physical hardware and energy infrastructure required to keep the AI revolution running.

While the threat of resumed hostilities remains a tail risk, the current market breadth suggests a transition from stagflation fears toward a growth-oriented recovery.

The FedEx Signal: What One Company Tells Us About the Broader Economy

FedEx Freight held its inaugural Investor Day this week, focusing on the upcoming separation of the freight unit into an independent, publicly traded company, which is currently on track for June 1, 2026.

One consistent theme seen in the managment’s comments was the transition from labor-intensive operations to a tech-first model designed to decouple headcount from volume. While the company celebrated its 40,000-member workforce, the underlying strategic initiatives (specifically dock optimization and automated billing) reveal a roadmap for mitigating labor volatility through digital substitution.

A standout metric is the company’s goal to reduce manual touchpoints in billing and invoicing by up to 60%. By moving away from complex, global legacy systems toward LTL-specific automation and bringing resolution tasks in-house or nearshore, FedEx is effectively insulating its back-office from administrative labor shortages.

On the docks, the deployment of DIM in Motion technology (capturing 90% of shipments in real-time) and RFID tracking has transformed the "handling unit" into a data point. This shift from weight-based to cube-based dimensional planning has already yielded a 12% increase in line-haul utilization. Machine learning tools now provide frontline leaders with real-time insights into "direct load" opportunities, resulting in a 10% reduction in physical handles.

For the financial markets, this is a clear play for operating leverage. By using AI and automated tracking to minimize the number of times a human must touch a pallet, FedEx is structurally lowering its cost-to-serve. In an era of "sticky" wages, this "silent" labor offset ensures that as demand returns, margin expansion can occur without a linear increase in hiring.

View From The Helm: Jamie Dimon (CEO of JPMorgan Chase)

In his latest letter to shareholders for JPMorgan Chase’s Annual Report (2025), CEO Jamie Dimon offers a sobering assessment of the global economy, urging leaders to look beyond deceptive short-term data. While acknowledging current "tailwinds"—including a $725 billion AI-driven CAPEX surge and resilient consumer balance sheets—Dimon warns of a potential "skunk at the party" in 2026: persistent inflation.

Dimon argues that while the U.S. economy is structurally more resilient and less energy-dependent than in the 1970s, it is not immune to a "tipping point." He highlights a dangerous confluence of "tectonic" risks:

record global sovereign deficits (hitting 5%),

geopolitical instability in Ukraine and Iran, and

a massive $1.8 trillion private credit market that has yet to be tested by a true credit recession.

"Interest rates are like gravity to almost all asset prices," Dimon notes, suggesting that any upward inflationary surprise could trigger a rapid flight to cash and a systemic drop in asset values.

🗳️ Reader Poll: The Vibe Check

How are you playing the "Ceasefire Rally"?The U.S.-Iran ceasefire has sent oil down and BTC up—but for how long? Tell us your move: |

|

Investor Takeaway

The current market environment is a study in contradiction: we are witnessing a massive relief rally fueled by a fragile ceasefire, even as the "gravity" of 3.0% Core PCE and Jamie Dimon’s warnings pull at the edges of growth.

While the "transformer crunch" and industrial automation provide a structural floor for the economy, the volatility in energy and Bitcoin reminds us that the "buy and hold" era has evolved into a "watch and adapt" era.

As we move into the close of the week, the winning play increasingly becomes more about identifying the high-conviction trends that survive the noise. It’s why many are looking toward curated, trend-driven approaches—like the automated Howard Lindzon Portfolio strategy on Surmount—which focuses on the specific momentum and public moves of seasoned investors who have navigated these cycles before. In a week defined by a "death cross" and a "Pakistan-mediated truce," staying aligned with proven conviction is often the best way to keep your bearings.